Summary

Gen Z is increasingly relying on “buy now, pay later” (BNPL) services for holiday shopping, with spending projected to rise 11.4% this year, totaling $18.5 billion.

These services appeal to younger consumers with limited credit histories but can lead to overextension, as they lack centralized reporting and encourage overspending.

Experts warn of accumulating fees, particularly when BNPL plans are tied to credit cards.

With inflation and rising credit card debt already burdening Gen Z, consumer advocates caution that these services may worsen financial instability despite their convenience.

When you think there’s no future, there’s no need to plan for one.

Gen Z knows that they’re gonna have bigger problems than debt.

What else are you going to do? Save for a house who’s price rises faster than you can earn money?

And meanwhile your bank or brokerage gets to play with that money for a real investment return

And the wage earner’s taxes will be used to bail them out when they make a bad bet

Yeeeup. Socialism for me, austerity for thee

One big recent consequence is it destroys credit short term, like less than a decade.

It’s recoverable, but every one counts as a new line of credit, which automatically gets closed about a year after payment.

So unless you also have a lot of zombie credit cards, it’s going to keep debt utilization waaaay up, number of accounts waaat up, and keep average age of accounts low.

This snowballs, especially if they ever do but a house. If they day ever comes, they’re going to lose alot of money again.

It’s like experiencing turbulence on a place so you scream YOLO and start playing Russian roulette.

If the plane goes down, it doesn’t matter. If it’s normal no big turbulence, then it’s just as much an increase in risk as playing on land.

They assume they’ll have bigger problems, and they may be right. But it’s should still be concerning.

We got a while before kids are unironically bumping this tho

This snowballs, especially if they ever do but a house

They know this will never happen. They’re not buying houses. They’re renting until they die on an overheated planet that no one wants to do anything about. Where one party rolls coal and the other pretends that the inflation reduction act makes up for the harm caused by the record oil production they brag about.

They know they’re fucked, and there’s no reason not to take on as much debt that they can’t pay back as possible.

(since no one can afford a house even with perfect credit)

They assume they’ll have bigger problems, and they may be right. But it’s should still be concerning.

Why isn’t this framed as predatory lending?

Because Capitalism demands exploitation

doesn’t mean we need to blame people (victims) rather than the organizations

Actually yes. Yes it does.

The poor are poor cuz they don’t work hard.

Can’t budget to help the homeless cuz some of them might trade food stamps for drugs.

If you didn’t want that baby you should have kept your lega closed.

Blaming the victim is as American as genociding the indigenous. Happens all day every day. Because this is the bad place.

It’s not just American, it’s very British too.

Klarna is a Swedish company.

Ah, the great American Dream. Pull yourself up by your bootstraps and work hard to

enrich the millionaires profiting off your laborearn that $0.12 raise you’ve been asking for.After ending genocide at home it just exports it.

I’m not sure because it definitely is.

The whole selling point of services like Klarna is they don’t show up on your credit checks, meaning you can very easily take on too much debt.

For the same reason that the subprime mortgage crisis wasn’t; line go up.

Eat, drink, and be merry, for tomorrow we die.

In this age where you can quickly spend thousands online (or even in person) without having to actually watch any of it disappear, and corporations are hiring psychologists to make their services and platforms as addicting as possible, you’re gonna get a lot of this

I see everyone in the comments saying that Gen Z have checked out and are waiting for the end but I really don’t think so.

I think it’s never been easier to manipulate a person to separate them from their money and things are deliberately designed that way. Big shiny upgrade now buttons, services forcing you onto 7 day free trials for premium plans upon signing up, expensive yearly subscriptions for products that ten years ago would have been unthinkable as anything other than one time purchases, you name it. Capitalists have used the internet to minmax their penny pinching.

to take this a step further, imagine someone who has been exposed to these services designed to be addictive their entire (digital) life, as well as being pushed further into these services by their peers who are equally addicted and the “influencers” they look up to that are paid by these services.

Yep. It’s seriously remarkable how deeply these fuckers have sunk their claws into our social fabric. Literally every possible tactic they can employ to suck as much money from as many people as possible, have been employed, consequences be damned no matter how severe. This cannot be allowed to continue

People do tend to learn defenses against the environment in, so Im surprised.

I swear on everything that I’ve read this article word for word years ago but replace gen z with millenials

Every single Millennial also had those predatory debit card overdraft fees.

Banks would allow them to purchase something even if the checking account had no money and then hits them with like 25$ for every overdraft. Practice only outlawed in 2010.

God It was this feeling of helpless anger when banks would screw you while u are down. Thanks Obama for fixing that.

Oh it was far worse than that…

They would actually change the order of your transactions in order to maximize the number of overdrafts (and each cost $30+).

For example, say you’ve got $80 in your account. You buy three separate meals over the course of Monday and Tuesday, and you’ve got $50 left in your account. But now you remember that there is that one thing they NEEDS to be paid for, but it’s $75 and you only have $50 on your account.

Well, you have no choice but to make the payment that brings you to -$25, and incur the single overdraft fee. Sucks, but $30 penalty is less than not having Internet for a month or whatever, so you do it.

So to recap: You had $50 left after those 3 meals. You made one single transaction that brought your account into negative, that means one overdraft fee, right?

Nope.

They would literally re-order the transactions, put the largest one first ($75), bringing your balance down to $5, THEN they would process the meals from Monday and Tuesday giving you THREE separate overdraft fees of $30 each.

So now you owe the bank $90 on top of the $25. And that was what the banks sold as, “overdraft protection.”

Shit was disgustingly egregious. Obama made it illegal I believe.

I wish this “overdraft protection” was opt in so people at least have a chance to understand it. I turn mine off, deny my card who gives a shit

Right, that’s how they fooled people for years. Any normal person would think “overdraft protection” means, “deny the transaction so you don’t overdraft.” But nope, complete opposite.

It was so scummy.

They wouldn’t let me turn mine off. The first bank flat out said no, the credit union charged me $5 to draft $100 from my savings. If there wasnt $100 in the savings, they would charge me the $5 to take what was in my savings and the $25 overdraft to cover the rest. There were no other options.

deleted by creator

We didn’t have this new term buy now pay later to the same extent, the millenials version just called credit cards credit cards.

“Buy now pay later” has been around for at least a decade. It wasn’t ubiquitous like it is now though. I knew things were bad when I went to pay for 2 pairs of shorts and they asked me if I wanted to stagger the payments. The total cost was $40.

Buy now pay later has been a thing since at least 2006 in the UK (I can find pictorial evidence for this with a flyer with “buy now, pay 2007”). But, I am quite sure I remember seeing this in the 80s and 90s too. For sure most large stores had their own credit systems that worked this way.

It’s not a new term, and actually I’m going to say that predatory techniques were more common in the 80s and 90s. People were definitely financially illiterate then too. Store credit was very common, I remember a very common APR was 29.9% with some pretty long terms on too. And the store credit system was of course designed in a way you could keep adding purchases, so you were ALWAYS paying this 29.9% year on year.

I think the only real difference was that with payments being far more physical without the internet. You could feel when you borrowed too much and people would cut back before reaching truly unrecoverable situations.

Point being, this isn’t a new thing. The virtualisation of everything I think has just made it much easier for young people now to get into situations they cannot easily get out of.

In the 80s and 90s you could easily get multiple credit cards. But usually you needed to go out and get them, or at least fill in paper based applications. There were also definitely less institutions offering them. So there was a real hard limit. Now there’s all kinds of ways to get credit. However, there’s few real large institutions at the top and I think they really should be coordinating centralised credit limits better.

My summary is, this isn’t new. Just the modern world has made it very easy to make it scale into higher debts now than it did before. That’s the only real difference.

The average youth of the 80s and 90s were not better at this IMO. (person that grew up in the 80s and 90s speaking here). There were just less opportunities pushed into your face.

You can get now that’s what I call music for 5 easy payments of 19.99!!

But I’ve not heard it called that until recently.

You don’t have an Aaron’s or Rent-a-center in your town? I’m a millennial and half my formative years were spent on a rent-a-center couch and bed. Half my belongings in my first house were rent to own, now that i think of it. I spent a lot more because of interest and scams but i had zero financial literacy then and i needed furniture. Without a credit card your options were/are limited.

I remember payday lending being a thing, rent to own on furniture rings a bell too, but I remember most of the focus being on credit cards and bank fees

PayPal had zero interest payment plans as far back as like 2010. I’m actually a bit surprised it didn’t take off sooner.

Basically reddit 10-15 years ago. The doomsday edging gets stale when you realize things are cyclical. Millennials were supposed to implode with debt by now. An economic cycles or two later and that didn’t happen. Now it’s Gen-Zs turn to be on the brink of doom.

Does it matter. It seems that a lot of them have checked out already as they see the world burning around them.

Hard to blame them.

lol time to write an article vilifying young people who somehow aren’t thriving in our flawless economic system. What self-indulgent idiots they are. Where’s my Pulitzer?

If were going to slip into a period of hyperinflation then taking on tons of consumer debt is just good financial planning.

This is correct, although usually you’d want to go into debt on something like housing but let’s be honest, that’s not possible. Why not pay an 80 dollar door dash across four payments?

Isn’t that only if wages increase alongside inflation

Oh no. If a fistfull of trillion dollar bills will buy you a shot glass of rice that maxed out credit card from the before time is pointless either way.

If $1,000 today is worth $5,000 tomorrow, you want to spend that $1,000 today so that when you pay up you only pay $1,000. Even if inflation hits you, you still only owe $1,000 no matter how much actual value those dollars still hold.

This is really interesting. Layaway purchases in stores used to be popular but went away in the late 90’s. It’s back now as BNPL, with much worse terms.

Layaway purchases in stores used to be popular but went away in the late 90’s. It’s back now as BNPL, with much worse terms.

Lawaway is superior. Laywaway had zero interest charges. Some places charged a flat fee, but you also didn’t get your item until the full balance was paid. There’s no chance of a lawaway purchase spiraling into a huge expense. The expense is fixed at the time of layaway and never gets higher. Lawaway also builds the ability to delay gratification, which is an important life skill that is sometimes not common.

BNPL has none of that consumer protection.

Correct me if I’m wrong, but wasn’t the key difference in layaway that you didn’t have access to the item until it was paid off? I remember my mom putting holiday gifts on layaway at Walmart. They’d be kept in storage in the back of the store, and would be given over only after they were fully paid off.

Buy now/pay later plans allow the consumer access to the item now, with a payment plan to follow. It’s much more akin to credit than layaway.

Yes. You had the honor of reserving the item from sale by paying more. BNPL is like the boss in its final form. You can have but don’t own it. Maybe it’s more akin to old furniture places with leases.

https://www.retailmenot.com/blog/walmart-layaway.html

Walmart actually just stopped layaway entirely in 2021 for BNPL.

In the UK the Littlewoods catalogue is the one I remember. You’d end up paying well over the RRP with a year or two of monthly payments.

deleted by creator

My credit card is just a proxy for my debit card, with benefits.

I thought everyone used theirs this way, I tell friends I have a credit card and they gasp.

Like wtf, it’s only as dangerous as you are. Use it, pay it. In, out. Ez pz.

It’s not just a matter of how big the purchase is. The you next year still who still pays for the car will also still be using the car. The you next month who still pays for the meal would have already pooped the meal.

Also I’ll add that there are some things that feel wrong that they just aren’t prepared for you to pay cash for. My audiologist was shocked when I asked him to put my hearing aids on a single debit payment and we had to break it up into three payments. My car was two payments one a day after the first. I was raised to save up for expenses where possible and avoid debt for anything but cars, houses, and education (and hoo boy did I get a lecture on expected income vs price of degree).

And I have to say that these issues are a combination of systemic and cultural. You don’t get this being so common with it being an individual failing, and you don’t get the situations I’ve described or the issues with debt avoiders getting screwed when we look to get a rare responsible loan without it being systemic. But also you don’t get people casually splurging with money they don’t have without it being cultural. Fiscal responsibility isn’t fun or sexy (though actually I have found a casual partner more attractive for the fact that she has retirement savings and minimal debt), but after decades of propaganda encouraging wasteful lifestyles and fiscal irresponsibility I think it’s time we engage in a multi prong approach to this problem. And that very much includes teaching the average American how to live a more frugal lifestyle while also making sure that they can get what they need (housing, transit, education, community participation, cultural enrichment, etc) at an affordable cost to their income.

Yeah, it’s pretty fucking insane the things people are taking on debt for. I genuinely can’t understand it. I mean, I know we live in a society that’s pretty fucked from capitalism and inequality and stuff isn’t easy, but it is common sense to avoid debt as much as possible. Do they just think the money is free?

Who is teaching them financial literacy in the first place? Because they aren’t being taught it in schools. Meanwhile, these predatory companies do everything they can to convince people to use them.

You cannot budget your way out of poverty. “Financial literacy” is just capitalists kicking the can down the road.

It’s not, though. Financial literacy includes things like, not spending money you don’t have. When you take these predatory loans to get goods, you end up more enslaved to the capitalist system and to those who have money to lend.

Financial literacy is not a cure-all, just like normal literacy doesn’t make you understand Shakespeare.

And they call them predatory loans for a reason. They are coming to you and they are going to hurt you. But we don’t teach kids this before they get into the adult world and this is the result.

Coming soon: Predator Loans Vs Loan Sharks

In cinemas just as soon as we pay off our bills.

Yeah, and financial literacy alone may not get you out of poverty, and it definitely won’t get everyone out of poverty, but among those with the possibility of class mobility financial literacy will play a role in where they wind up.

I think it is highly unlikely that all of the Gen Z people getting these loans came out of a life of poverty.

deleted by creator

Cool, except I was very clearly talking about the financial literacy to not do things like get suckered by a predatory lender.

Why are you against that?

This is the level of discourse at this point. Someone makes an observation or a comment and people think responding with a meme is a “gotcha.”

No wonder everything is fucked.

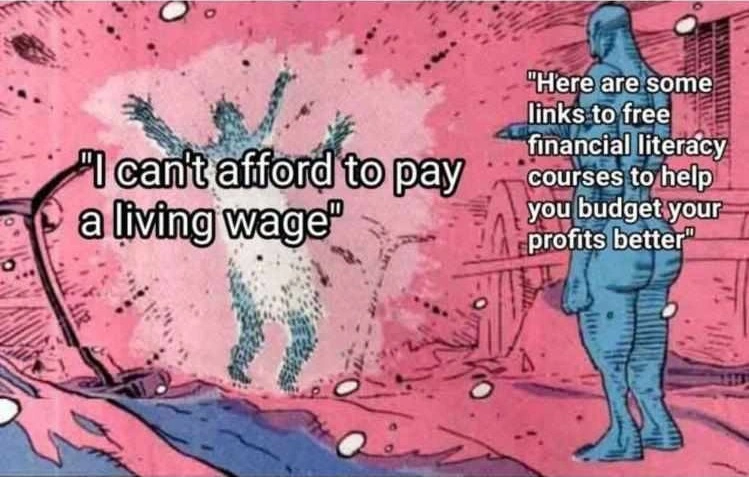

The label on the on the guy being explode talks about paying your staff a living wage. Basically, it’s a dunk on arguments that raising the minimum wage would loose jobs.

And it had absolutely nothing to do with what I was talking about besides the term “financial literacy.”

If you don’t think it’s sensible to teach young people to avoid predatory lenders before it’s too late, just say so. Otherwise this is irrelevant.

Stuff like this is why the headline Econ stats do not actually reflect reality.

Sure, there’s lots of room for critiquing how the media and the investor class focus on stats that are not actually representative of things on the ground for fairly complex mathematical/economic reasons, but that conversation requires people to have a Masters on Econ to understand.

What does not require this is the much simpler: They do not take personal debt levels and credit scores into account.

People say things like ‘inflation is going up’ ‘i cant afford as much as i used to’ and … the main actual reason for this is usually that they’re drowning in debt, but are either unaware or don’t want to admit it.

This is a country where 54% of adults read and write at below a 6th grade level. Probably a comparable amount can’t actually do their own budget.

…

It doesn’t matter if your wages go up 2% in a year if you had to spend that year buying groceries on credit to not starve, and those all have 16 to 36% interest rates.

Systemic issues can only be solved with systemic changes.

No amount of shaming individuals will fix systemic debt issues, if this is such a large trend that it effects most of the generation then it can only be fixed with systemic changes.

The narrative that individuals are responsible for widespread debt is propaganda meant to shift blame off of the rich people causing wealth inequality to skyrocket

I don’t think their comment was about shaming individuals, but rather pointing out that there are individual level factors that economists don’t take into account when measuring economic health.

Its not even ‘individial factors’ in the sense that everyone faces unique situations that are not captured by data.

These credit / debt amounts are obviously captured by credit agencies, banks, etc., sold off to data brokers, either anonymized or not.

How else would any credit check occur?

A BLS economist could easily work these in to existing top line numbers, or make a new headline index.

Income Sans Recurring Debt Payments (car, house, consumer debt, student loans, etc)

Average

Median

Percentiles / Buckets / Brackets

Household/Individual

By Age

By Sex

By Location

By Gross Income

By Education Level

…etc.

The data is there. The math is not that hard (for an Economist or Data Scientist).

They just don’t.

It’s lieing by ommission.

I wonder if this research is done but not picked up by media.

I’m honestly not sure. I have the means to check but not the time-energy, unfortunately.

Maybe a few times a year a story makes it fairly mainstream in terms of internet news, but it almost never trends amongst popular streamers / youtubers / podcasts, or airs on TV.

Credit Karma or some other credit agency, or maybe some non profit or academic research will show up, as this article is…

… But the data obviously exists to be able to study and work into a new metric, which could be reported probably at a monthly pace, worst case, quarterly.

Lies, damned lies, and statistics.

The BLS does, I think? have some very rough aggregate stats on consumer debt levels, but nobody reports on it the way business news orgasms every time the jobs print and CPI come out…

Systemic issues can only be solved with systemic changes.

Blaming any individual for their outcome in a system that creates these issues distracts people from the cause of the issues, wealth inequality.

That’s why choosing to obsess over individual choices is totally useless and literal propaganda keeping people from correctly focusing their frustrations

No clue how you read myself shaming individuals into what I wrote.

I was writing to explain why everyone feels poorer than all the headline Econ numbers say we should feel.

Why all the libs who spent the last year or two telling us ‘the economy is fine actually’ were just factually wrong, functionally gaslighting everyone.

If anything, I call out the media, media friendly ‘economists’ and business people for perpetuating bullshit.

Obviously a general explosion in personal debt levels is a general, systemic problem with systemic solutions?

…

I am all for systemic solutions:

Tax the Wealthy / Tax Corporations

Get rid of student loans, do free tuition

Do a total debt jubilee for those below I dunno 200% poverty income threshold

Cap all consumer credit instruments of all kinds at 3x the Fed Rate

Raise the threshold of income for SNAP and LIHEAP and EITC, etc

Implement universal healthcare, outlaw private insurance, lower costs

Raise the minimum wage

Rent control, automatically expunge all eviction records after 1 or 2 years, actually fund building public housing, write a law that says if a house or condo is on market, unsold, you must drop its price by 5% for every 3 months it remains unsold…

Blah blah, tons of things we could theoretically do.

Only systemic changes will fix systemic issues.

… Are you a bot, or do you just have extremely poor reading comprehension?

Can you explain how me stating that a whole bunch of people have a lot of debt … implies I am blaming them individually for this?

If I told you that black men are much more likely to be sentenced heavily for the same crimes, abused or killed by cops… would you think that means I am implying that that is their fault?

If I told you that trans people have higher suicide rates… am I also implicitly saying that is their fault?

How…are you reading a causal or morally prescriptive blame into these statements that are just data, just statistics… after I have already stated that obviously these are systemic problems that require systemic solutions?

If you understand that these systemic issues will only be solved by systemic changes then that’s it.

Idk why you keep replying

I mean, we’ve been telling them their entire lives that the planet is doomed, and they have no future… So why the fuck not bring on the debt?

Because rampant over consumption is the reason the planet is doomed.

There is no ethical consumption while living a capitalist way of life.

It isn’t a black and white issue though. There is more ethical and less ethical, but less ethical tends to be cheaper and easier.

The entire idea that individuals are responsible for these systemic issues is propaganda meant to distract from the rich who actually cause the problems

The responsibility is shared. Temu wouldn’t exist if nobody bought from them. Yes, people need clothes, but nobody is forced to buy them from a fast fashion company that is generating enormous amounts of waste. 🤷

Systemic problem can only be fixed by systemic changes, no amount of fixating on individuals will ever fix a systemic issue

True enough, as is the visit it before it’s gone. Yes, the Great Barrier Reef is dying from emissions and the resultant rising temp but fuck it, fly across the planet.

I’m going to be brutally honest.

- Corporations are shitstains and prey upon people’s minds and wants.

- People today are too entitled / greedy.

No. You don’t need that phone to survive, solid but low end one will easily carry you next 3-5 years. No, you do not need to go for McD for breakfast - eat a homemade sandwhich. Takes the same amount of time it’d take to get McD served to you.

But today a lot of folk take a lot of shit for granted or worse, needed, and it’s pitiful.

Fuck, that also is due to corporate ads and framing. But people need to wake up and stop fueling this shit on their own. And stop blaming schools - this shit is for parents to teach ffs, like the rest of actual household chores.

Also I am not arguing for everyone to live frugally but instead to learn a mindful way of spending. If you actually have free money, money you own and not a credit, then sure, treat yourself.

It’s something I don’t understand. Writing this on a 5 year old phone that cost me 130 euros back then. I do have the money to buy any reasonable phone on the market (not some vanity ones for rich people to show off, but like the top of the line iPhone or Pixel, whatever).

But why would I when the old one still works and does everything I need? Why would I order food when I can just make something myself? If I want to treat myself, I go to a restaurant that I actually like and spend like 30 euros tops. That’s once every one or two months. Why do people overspend on this?

If you have kids and actually struggle with basic goods, that is something completely different. But I get the point you’re trying to make - some people just feel entitled to a standard of living that they can’t afford, and corporations gladly exploit that. And honestly, they’d be stupid not to. A sucker is born every minute. It’s up to the legislative to stop this predatory behavior because the market won’t regulate itself in this regard.

And you’re right, it’s not up to school to teach this - I wanted to comment on this one as well - school is supposed to turn you into a person that can think for yourself and realize that a high interest rate is something to your disadvantage. Not to exactly tell you what to do in situation X should you ever encounter it. Because society and its problems change and then suddenly what you learned no longer applies.

In the end, I can’t tell people how to spend their money. But once might make the case that with BNPL, people spend money that’s not not actually theirs yet. And once these people need help, is going to be society to foot bills, not the corporations who made money off it.

Systemic issues can only be solved with systemic changes…

No amount of shaming individuals will fix systemic debt issues, if this is such a large trend that it effects most of the generation then it can only be fixed with systemic changes.

The narrative that individuals are responsible for widespread debt is propaganda meant to shift blame off of the rich people causing wealth inequality to skyrocket

There is propaganda and then there is fact that nobody teaches their children about budgeting and financial responsibility. Do not treat credit like money you own, do not allow yourself to perceive luxury items as something you need, be mindful of what you can actually afford. Today people seem to have problems with these ideas - lack of education on the topic and aggressive ad campaigns by corporations resulted in that.

But while we cannot change masses, we not only can, but we should point this out to as many people as we can. Often all you need to notice something is for someone else to ask question about why that happens. And yeah, sure, maybe helping one or two people won’t make a dent, and even then these people may already be past saving or simply unable to pick up new habits. But if every mindful person tries to help someone else at least once, shift in society is guaranteed. And such shift will result, maybe, in actual change.

And, on a more flat approach - being aware of your own budgeting limits, spending power and how much money you use is not actually yours tends to radicalize people against the rich.

Only systemic changes can fix systemic issues .

This widespread propaganda needs to be countered with grassroots encouragement of more practical relationships with money though. That’s the cultural onus for systematic change. Don’t just shame them, but encourage everyone to live more responsibly and to vote for people who will reign in the creditors spreading this propaganda and loaning easy money to every financially irresponsible person

Without grassroots cultural change anyone who reigns this shit in will face political suicide for taking away their easy lines of credit. We see similar things with things like carbon taxation and other incentives to reduce carbon emissions that involve reducing overconsumption by all people (because yes, the average American is part of the problem too). The elites need to lose the most, but all of us need to live a financially and environmentally sustainable lifestyle and the systemic changes we all talk about wanting will impact our lives.

Only systemic changes will fix systemic issues

Oh wonderful and I suppose we should do nothing to bring those systemic changes about too? No systemic changes begin with changes to our community mindsets. The big creditors want you to not be talking about how they’re propagandizing to convince you to take easy lines of casual credit for fun little splurges and that that’s a trap and you shouldn’t take it. They want you to think that it’s not worth saving money and living within your means and they want you to keep up with the joneses and to make your friends uncomfortable not doing so. And most importantly they want people to feel like any expectation that they shouldn’t get instant and constant gratification is an unacceptable cost. When they get their way systemic change is infeasible. When they are seen as parasites lying to the masses and tricking them into living beyond their means, systemic change becomes possible. Politics are downstream of culture. You can’t change the policy neatly as easily as you can change the minds of those around you

Pretending like individual choices would do anything ignores the fact that these systemic issues can only be fixed with systemic changes

No amount of financial literacy will fix income inequality, we need to redistribute wealth if we want everyone to have the proportional wealth to participate in the economy.

I hate BNPY so much… I deleted my after pay account, which means I can no long use their services unless I get in contact with support to reopen my account. I did it to explicitly make it near impossible for me to be tempted. It worked. There were times I felt regret, but it was 100% the smartest move.

Then, PayPal introduced pay in 4… All my hard work went right down the drain. I can’t afford this shit but fuck it’s hard when you’re clinically depressed.

Services should be required to allow you to opt out of being offered such things. I choose to live a debt minimal lifestyle because of how I was raised, and I don’t want to be tempted. The same goes for online gambling. (And alcohol advertisements, but I do drink).