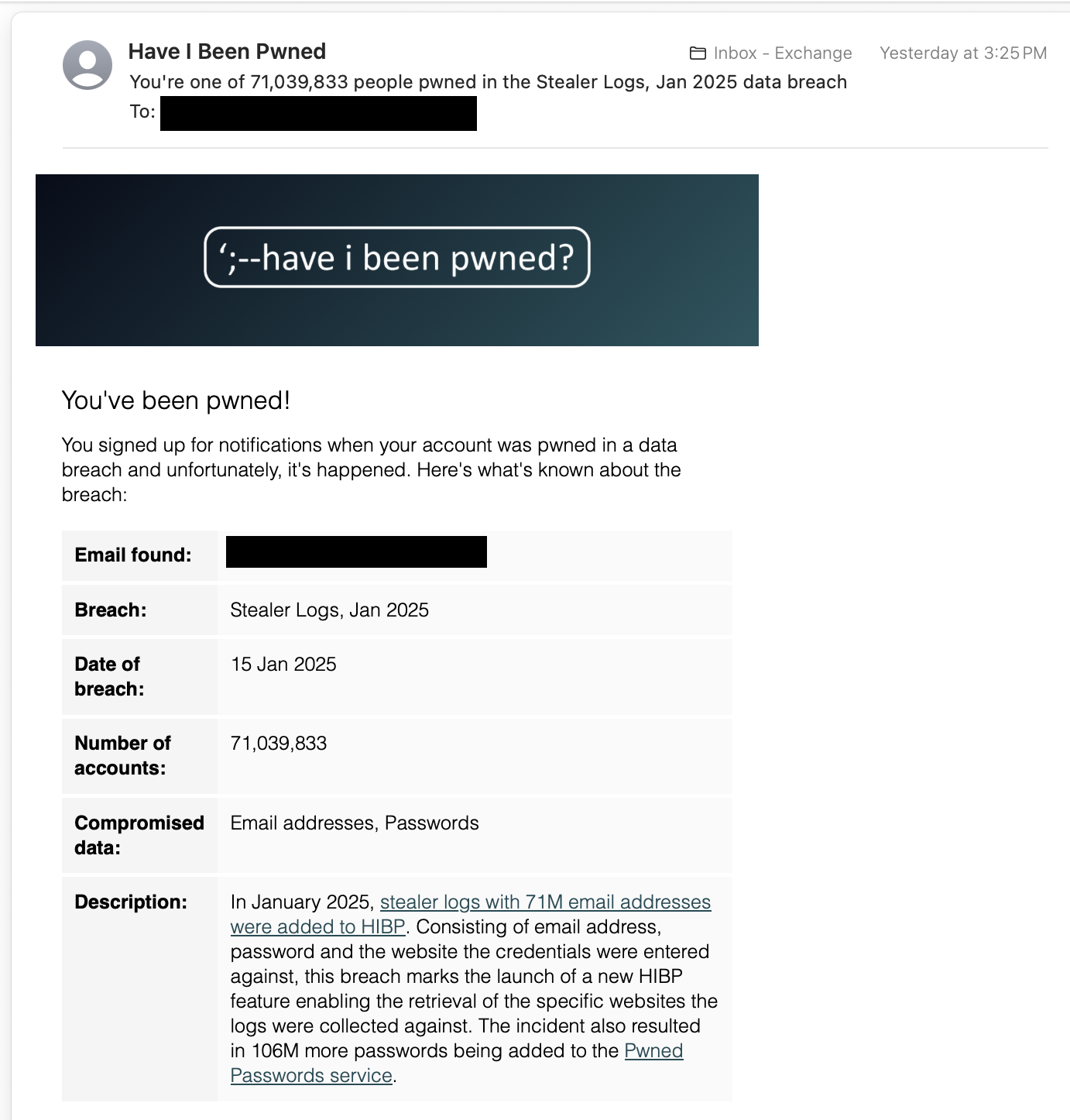

Password manager, and use different randomly generated passwords.

The real danger is having the same password everywhere.

Also pay attention to where you save your payment info.

Everything I do online is through Privacy.com, with limits for each vendor. My amazon gets hacked? Most I’m out is $100, steam gets hacked, there goes $60. A subscription tries to double charge, lol no. Free trial wants to auto-bill me after 7 days, its not happening.

Funneling everything through them isn’t 100%, but at least they’re not paypal, I get notified when ever even a 1 cent charge happens and I’m not leaving my bank card on a dozen random sites I’ll eventually loose track of.

Another thing you can do is to keep available funds on whatever card you use online low. If there’s only 1 to 2k on the card, yes it’ll suck, but it won’t be as impactfull as your life savings.

You a might also consider credit card with a small limit (1k or less) and set auto pay to “pay full balance” every month. Avoid interest like the plague, (those cards have insane interest rates over 20%), but if you’re always paying it off in full, there’s no interest to pay.

If I can’t pay the credit card off in full (and I mean the full limit) when I “swipe” it, I pretend it does not exist. None of the “I get played next week, so I can pay it off then” - nope, don’t go there.

Supposedly credit cards have better fraud protection than a debit, but maybe that’s just another one of our many “Freedom” problems.

The main thing is you’re separating the random websites from the majority of your funds to limit how much can be taken.

If there’s a problem, I’m dealing with Privacy.com and a couple hundred bucks and can still pay the bills. I’m not trying to convince ebayclone#71 and my bank I didn’t place an order for 10000 waffle makers before the lights shut off.

And of course, I’m just some rando on the internet, not an actual expert. Not even in same country as you, so take that for what it is.

I wouldn’t recommend keeping credit card limits low to only mitigate fraud risk - credit card companies generally will take the hit for unauthorized use, aka stolen information, and send you a new card. So keeping the limit low in an effort to make sure that if your info is stolen they’ll only be able to steal $1000 or $2000 isn’t really necessary, and only affects your ability to use credit and have a better credit score (because your % of utilization of your overall credit limit goes into your FICO).

Instead, review your purchases monthly and inform the card company of charges you didn’t make as soon as you see them.

DEBIT cards are a different story. They’re a direct link to your bank account funds and there’s no intermediary that is willing to take a hit, it’s your bank vs you, so if your debit card info (and pin) are exposed you’re much more vulnerable. So I wouldn’t recommend EVER using debit these days, there’s zero reason to, but if you have to then your advice in your OP is more appropriate.

You don’t need a credit card for most things in Europe so it’s not as pressing. Even if a company leaked my bank account details, no one can charge it by default.

It’s not that you change the passwords for each website often, it’s that you use a different password for each site. That way if one site gets hacked and your password is leaked, it can’t be used to access your accounts on other sites.

{kind=link}

Password manager, and use different randomly generated passwords.

The real danger is having the same password everywhere.

Also pay attention to where you save your payment info.

Everything I do online is through Privacy.com, with limits for each vendor. My amazon gets hacked? Most I’m out is $100, steam gets hacked, there goes $60. A subscription tries to double charge, lol no. Free trial wants to auto-bill me after 7 days, its not happening. Funneling everything through them isn’t 100%, but at least they’re not paypal, I get notified when ever even a 1 cent charge happens and I’m not leaving my bank card on a dozen random sites I’ll eventually loose track of.

Sadly I don’t know of an alternative operating in Europe.

Revolut? I think you can create cards the same way

I do this. However I also hit the limit of disposable cards.

Turns out to not be as many as I would have thought.

Didn’t know that! Not using it but I heard you can then they decided to ban more secure custom ROMs 🤷♂️

That’s unfortunate.

Another thing you can do is to keep available funds on whatever card you use online low. If there’s only 1 to 2k on the card, yes it’ll suck, but it won’t be as impactfull as your life savings.

You a might also consider credit card with a small limit (1k or less) and set auto pay to “pay full balance” every month. Avoid interest like the plague, (those cards have insane interest rates over 20%), but if you’re always paying it off in full, there’s no interest to pay. If I can’t pay the credit card off in full (and I mean the full limit) when I “swipe” it, I pretend it does not exist. None of the “I get played next week, so I can pay it off then” - nope, don’t go there.

Supposedly credit cards have better fraud protection than a debit, but maybe that’s just another one of our many “Freedom” problems.

The main thing is you’re separating the random websites from the majority of your funds to limit how much can be taken. If there’s a problem, I’m dealing with Privacy.com and a couple hundred bucks and can still pay the bills. I’m not trying to convince ebayclone#71 and my bank I didn’t place an order for 10000 waffle makers before the lights shut off.

And of course, I’m just some rando on the internet, not an actual expert. Not even in same country as you, so take that for what it is.

1k or 2k? Lol, my debit cards only have $20 at a time on them at max.

I wouldn’t recommend keeping credit card limits low to only mitigate fraud risk - credit card companies generally will take the hit for unauthorized use, aka stolen information, and send you a new card. So keeping the limit low in an effort to make sure that if your info is stolen they’ll only be able to steal $1000 or $2000 isn’t really necessary, and only affects your ability to use credit and have a better credit score (because your % of utilization of your overall credit limit goes into your FICO).

Instead, review your purchases monthly and inform the card company of charges you didn’t make as soon as you see them.

DEBIT cards are a different story. They’re a direct link to your bank account funds and there’s no intermediary that is willing to take a hit, it’s your bank vs you, so if your debit card info (and pin) are exposed you’re much more vulnerable. So I wouldn’t recommend EVER using debit these days, there’s zero reason to, but if you have to then your advice in your OP is more appropriate.

You don’t need a credit card for most things in Europe so it’s not as pressing. Even if a company leaked my bank account details, no one can charge it by default.

What if my chosen service doesn’t allow me to change passwords that frequently?

It’s not that you change the passwords for each website often, it’s that you use a different password for each site. That way if one site gets hacked and your password is leaked, it can’t be used to access your accounts on other sites.

Also a note that captial one has a similar service for their own credit cards. Def not as good as privacy.com, but still useful.

Good to know.